After the failed attempt, for now, of Deep yellow to takeover Vimy resources, I thought I would share my latest thinking of that transaction and more possible targets for DYL. The below was written a full week before the announcement. I have to admit that I had many laughs reading all the Vimy shareholder’s responses to that takeover bid!

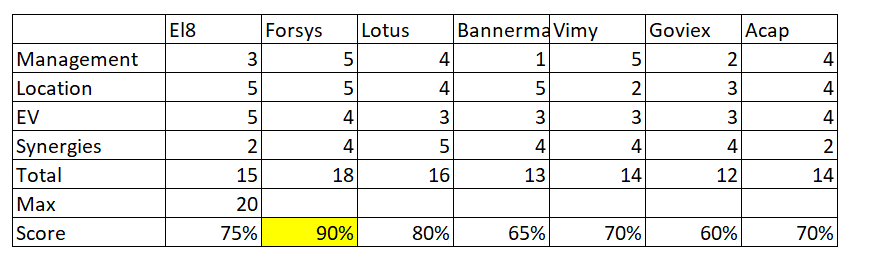

Let discuss which companies could be the best candidate to take out by looking at the following 4 criteria and giving a 5 point rating scale to each of the criteria. 1 being the lowest and 5 being the highest to see which project has the most potential to be taken over.

1-Management strength

2-Project location

3-Market caps

4-synergies

5-other areas to unlock shareholder value

Companies in Focus: FSY, EL8, Bannerman, Lotus, GXU, Vimy, A-cap,

When looking at management, I think the weaker the management and the better it makes for a potential takeover. The reasoning is simple, if you have 2 top CEOs, it becomes a problem to let one go or said otherwise, it becomes more probable that the Ceo that is being taken over does not exactly want to leave his position making the deal less likely.

Forsys and Vimy have no management to speak. Therefore, they are a 5. Almost a perfect target. On the other hand of the spectrum, Bannerman has a leading/Elite Ceo. This makes it harder to foresee them as a takeover. Therefore, it’s a 1. Lotus has a new Ceo and A-cap has a uranium project that has been on the shelves for almost a decade. Therefore, they are also great takeover targets and will give them 4. Daniel at Goviex is experienced and keeps pushing the projects forward. Hard to say if he is a 2 or a 3 on that scale but I will give him a 2 here. I would put Murray as a 3 because he is great at what he does but I am not sure he could take the project all the way to production. That being said, he does not need to.

Project location

here, I would say the closer to the existing project from Deep yellow would be the best. We should also think about the mining jurisdiction if the project is not in Namibia. To Bannerman, Forsys, and Elevate, we should give 5s as they are neighbors to the deep yellow project. A-cap’s Botswana project is the next closest nearing also the Lotus’Malawi project which we should give a 4. Then we get Goviex in niger, mail, and Zambia which is also in Africa but the distance is quite vast. Might as well say it is as far as Vimy( for the NIger and Mali part). However, we need to consider that Niger is more Uranium friendly than Australia. Therefore, a 3 to Goviex and a 2 to Vimy since they still have a license, one of only 4, in Australia for a uranium project.

Enterprise Value

The idea here is that the lower the Enterprise Value, the easier it is to be taken over. Therefore, we go with a very mathematical approach. (The first Column is EV in USD Millions)

GXU: 182MUSD LBS: 209M EV/LBS: 0.87$

FSY: 140MUSD LBS: 216M EV/LBS: 0.65$

EL8: 81MUSD LBS: 94M EV/LBS: 0.87$

Vimy: 201MUSD LBS:158M EV/LBS: 1.26$

BMN: 177MUSD LBS:270M EV/LBS: 0.66$

ACB: 131MUSD LBS:365M EV/LBS: 0.36$

Lotus: 194MUSD LBS:37.5M EV/LBS: 5.19$

DYL: 232MUSD LBS: 185M EV/LBS: 1.25$

Elevate gets a 5, ACB and Forsys a 4, BNM GXU, Lotus and Vimy get a 3. All companies have smaller Enterprise value compared to Deep Yellow.

Synergies

Synergies in the uranium sector, in my opinion, are mostly related to the duplication of teams. If there are roughly 70 miners, developers and explorers total, that each of these management teams earns roughly 1m-2m in salary and stock options, then you are looking at 70m-140 in wages and salaries per year for the Uranium sector. Then there is the office, consulting duplication travel, and overall SG&A. ( Selling, General and Administrative expense) For the sake of this conversation, nothing scientific but let get another 1m per year per company. The total hunting ground of savings for the total industry would be in the area of 140m to 210m per year. This is essentially what you can reduce and can enhance the value of acquisition for the acquirer. In the current case, Deep Yellow would also benefit from having higher production than their current DFS for the Thumas project suggest. Their operating production capacity per year is 3m lbs of Uranium per year. Knowing that Kazatomprom produces about 60m lbs per year, that Cameco can produce 20m to 30m lbs when McArthur River is brought back online, to anyone in the sector, it will be important to gain scale to stay competitive. Paladin should be able to produce 6m-7m lbs a year, Global Atomic should produce between 4m-5m lbs per year, Boss energy planning to produce 3.3m lbs per year, Lotus with 3m lbs a year, I would assume that Deep Yellow would like to get in the top producers as they become more attractive to contract with from a utility standpoint. Bigger and more stable production will increase the confidence of delivery to the utilities

In this ranking, let’s look at who could bring the most scale and highest synergy.

Assuming that they would only buy the Namibian asset, El8 would add considerable reserves to Deep yellow but no real synergies to speak of. The same could be said for A-cap’s deposit. Therefore, I would give them a low ranking of 2. Assuming a full takeover of the rest of the companies, you would get more synergies and also the resource upgrade. I would give them all a good 4 score. The only one that stands out as having a bigger impact on DYL would be Lotus as they are operation ready with a very low restart CAPEX. If you add to the mix the fact that JB operated the deposit while he was at Paladin, I would give this the highest possible score of 5 because of the familiarity of the operation.

Other considerations

As you are reading this, you might notice that this feels outdated as DYL made a hostile takeover offer, giving 72 hours to VIMY resources, to respond to their offer on November 15th. I left the original write-up as a way to remind ourselves that while forecasts are important to our thesis, they will not happen exactly as we have predicted. I will go back later on the Vimy hostile takeover. A few of you were quick to remind me that JB has mentioned many times over he wanted to grow DYL as a multi-jurisdiction company but would stay away from countries that had no prior track record of Uranium mining. That would then decrease the likelihood of buying A-cap energy as Botswana does not have a long-standing Uranium history. Lotus, which was sold off by Paladin, also resides in a jurisdiction that has a very novel history regarding Uranium mining, therefore, I would also be keen to give that a lower grade than say projects in Namibia, Niger, and Australia.

I would also like to think about this transaction in terms of what is it that you are adding to Deep Yellow? Expertise? Bigger resource? A mill? A turn-key project? John Borschoff is arguably one of the most experienced executives in the sector. He took Pallading from an explorer to a developer, to a producer in more than one jurisdiction whilst managing also to do some significant M&A. Therefore, in his case, I am pretty certain that he is not looking for more or better expertise. A bigger resource is important especially if the ambition is to supply utilities and become a long-term partner. As many in the sector have pointed out, utilities value the trust of supply probably higher than the price they will pay. Furthermore, it is easier to deal with fewer and bigger sellers than many small ones. Deep Yellow does not need per see to have a mill. They are blessed with having Hussab and Rossing next door and a plan to build their own. A turn-key project? If that was the case, JB would be looking at Lotus, URG, LAM who have assets that can come back online within 12 months however, it looks like this is not his strategy.

The last thing on my mind is to say, what will you be paying for that? Or said otherwise, what is the value that you are getting for the acquirer? An over-simple valuation metric used, but definitely not the best, by all means, is the EV/lbs. I have shown these values above using the Measured, Indicated, and Inferred lbs. There is a much bigger premium on Lotus given that the project is significantly derisked. It also gives you an idea of what the market is willing to pay for pounds in the ground. The smaller EV/lbs compared to the current valuation of DYL can signify that the company could generate increased equity value simply by adding a bigger resource. The equation is as follows: every 100m lbs of increased resource, at the current multiple, would increase the equity value by 125m whereas if you look at Forsys as an example, the current resource is only valued at 0.65$ per lbs meaning DYL could generate an extra 0.60$ per lbs on increased valuation multiplied by the 200+m lbs which are roughly 120$m of increased equity value. Does that mean it is a given? Absolutely not. Forsys’ project has been idle without management and would need to review its financials since they are outdated. The market is also hinting at that with its lower valuation.

What is next

If you have been keeping score, I still think that Forsys and Elevate would bring the biggest value to Deep Yellow. It seems however that John B does not agree as the recent takeover bid for Vimy was submitted. Where do we go from here? The most probable next step will be to increase the bid for Vimy. How much more? in the last bull market, we had seen developers peaking at 4$-5$ of EV/LBS meaning that Deep Yellow could potentially almost double their bid, think around 0.5$ AUD per share, and still have plenty of valuation upside assuming that the bull market keeps running as we expect it to be.

What do you think happens next? Which M&A would you like to see and why? What do you think I am missing in the above scenarios?

I always love to hear from you guys!

cheers,

Max

reposting my thoughts here:

You got "unlucky" on your post timing a second time, or maybe it's lucky :) DYL released an announcement ~6 hours after your article restating their position and their interest in VMY! It pretty much confirmed your "what's next?" section's accuracy. Looks like they are quite intent on Vimy, but also looks like JB is determined not to raise his offer too much (or at least wants to appear that way).

The fact it's a 100% scrip bid does alleviate a few of the factors that might necessitate offering a larger deal-sweetener, too - all the bullish arguments that apply to to the shares of VMY that shareholders are being asked to surrender, apply pretty much equally well to the shares of DYL they are being offered as compensation. As for what's a fair offer, it would take a more dedicated and knowledgeable numbers guy than me to work that out, but consensus among names I respect on twitter seemed to be "JB can offer more than a 10% premium here and still have it be solidly accretive to DYL holders".

Gut feeling is that VMY holders definitely would want (deserve?) a bit more of a compensatory sugar hit than 10%, because while for DYL holders their exposure is changing a little, it's in line with what their CEO told them to expect, it's what they always planned. For VMY holders, they are suddenly asked to go from a pure simple permitted open pit WA play to accepting large exposure to a diversified very early stage Namibia jurisdiction developer, with a rockstar premium on management. Or at the other end of the spectrum, people like me who are already irresponsibly exposed to DYL and aren't necessarily looking to add :)

Both those groups are perhaps 'forced' to sell and realise capital gains they didn't want to realise yet - in my case if I do so I will also be somewhat narrowly missing out on the 12 month CGT discount, so likely my gains will be taxed 45% instead of 22.5%. Yes, that's a personal circumstance, but it will not be a unique one and it will influence how retail holders perceive the offers, to the degree to which that affects anything (perhaps not much, I admit)

If I were JB i'd call sprott and the Friedlands and have them help me buy all of the above but ACAP. Make the OPEC+ of Uranium in concert with $SPUT. Let Munro market, JB develop & corner the market.