Interview with Energy Fuels

Interview with Energy Fuels

a great discussion with Mark Chalmers and Curtis Moore

Hi Everyone,

I hope that you had a great weekend! It’s a rainy bank holiday in Ireland today which is great after all the work we did in the garden. I am crossing my fingers that the transplanting of our peppers, cucumbers, radishes, green beans, beets is successful.

We had the pleasure of meeting up with Energy Fuels’ CEO ( Mark Chalmers) and VP of Marketing ( Curtis H Moore) last week and I wanted to share the details of this conversation.

Specifically, we will elaborate on these 3 topics:

Current Macro environment in Uranium

Rare Earth Project

Disposal of non-core assets

Macro view

We asked Mark to give us his views on the current market view in the uranium market. He liked the recent market since December which obviously benefitted his company but increasing their Market Cap by 200% since late November. This market allows for easier financing which they faced in the last couple of years and insufficient means to finance means reduced ability to explore and acquire properties. The ongoing low price in uranium also means that most of their mines are under care and maintenance and with a cash burn or 1.5million per month and 94 full-time employees, Energy fuels needs a turnaround in the Uranium price more than certain peers. Their current balance sheet position does not allow them to have a further prolonged softness in the market otherwise they will need to dilute investors furthermore without increasing the value of the company. Scratch that, since I am looking at the full-year audited financial statement. Energy fuel issued 5.5 million shares between January to March 2021. This would bring their Cash reserves to approximately 50 million USD and an additional 30 million USD worth of inventories of finished goods.

On the topic of utilities signing long-term contracts and the psychology of the utility buyers, I think Curtis gave us the most interesting answer I have heard to date. Most utility buyers receive generous state subsidies. These subsidies need to be renewed every so often. The greatest fear that utility buyers have is to contract long-term while it is still possible to buy, albeit much smaller quantities, uranium on the spot market for a lower choice. They absolutely do not want to go back to their state representative, which themselves are elected every few years, and ask for ongoing subsidies if there is a way to get them cheaper. Utility buyers do not receive bonuses because they might have procured uranium at a better price than the spot market but they save themselves the embarrassment or said otherwise, their elected representatives will save face. Understanding this is key to forecast when utility comes back to the negotiating table. On the one hand, someone like Energy fuels needs 50$/lb of uranium to restart production and on the other hand, utility buyers do not care to pay 100$/lbs as long as everyone else in the market pays the same price. Who will budge first? We can make an educated guess but with the news that Sprott bought UPC and will manage it as a new Uranium physical trust, somewhat as they do with the physical silver and gold trust, this might entice utilities to review some of their long-term strategies. When I asked them about restarting iddle production, they said that 50 million would be needed and about a year to ramp it up. This is quite similar to the likes of Boss Energy, Paladin which would equally produce 1-2 million pounds per year. On the question of further dilution, Curtis and Mark gave us the typical answer “ we will see where the market is for financing” but they did not feel like diluting another 50 million, which is roughly 6% of the current market cap would be something the market would not be happy to diggest. I interpreted that as, if their share price stays roughly where it is, they will not look at debt to fund the restart of the operation and who can blame them? In terms of potential M&A, his comments were that he is always on the lookout but thinks he already has the best in class projects and is currently trying to divest non-core assets. My read on the topic is that they have their hands full with bringing the rare earth business online and M&A is not top of mind. Any acquisition would also mean more dilution on top of what is needed to bring current production online. In lament term's term, I just don’t see Energy Fuel consolidating the market in the next couple of months.

Rare Earth

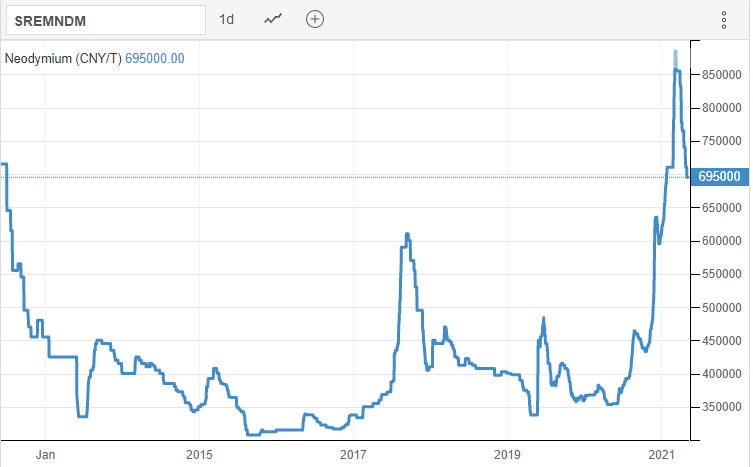

I will not dwell so much on the rare earth piece as Mark has already given plenty of interviews about the business case. Instead, I will answer some questions that were proposed on the blog/Reddit. On the question of capacity, the white mesa mill, as I understand, is quite big and can easily accommodate the rare earth and the uranium businesses. Reading my notes, I should have asked if they can run both at the same time but they mention that the monatize would only take roughly 5% of the mill capacity. I take it that it would be possible then to have both businesses running simultaneously. On the subject of profitability, Curtis says that they cannot beat a Chinese state-owned supply chain but will be able to be competitive outside of China. Their claim to fame is that they say they achieved more in the last year than any other companies outside china have. On that statement, it is true that they have been constantly in the news making deals with companies in the USA to get the monatize, in Estonia to separate the ore, with the Us department ad Penn state on getting a grant to develop the project. Is this the fastest development, I can’t tell but they sure have a great marketing tactic behind the rare earth business which should not be understated as an asset. Too many small companies can’t get on investors’ radar because of the lack of clear communication which is not an issue here. How long does that take to bring to life as a fully running business? Not before 2023-2024 therefore, not something we should expect to generate significant cash flow before 2025. What is the biggest hurdle to bringing this project to life? Price of rare earth metals going down. Currently, Neodymium, one of the most important rare earth metals has had sustained high prices which entices production. We need these prices to stay where they are to continue this venture in a sustainable and profitable way. How much will they need to spend to prove the business case? They believe the case is already proven but would need another 1-2 million to prove to the market that they can do it. Where do they see this business in comparison to uranium? The third pillar of revenues after Uranium and Vanadium. What is the end goal? 5 billion-dollar company or 20$/share price. Are they lobbying in Washington? I did not get an exact answer besides saying they have been very active there are keeping busy. Does the current team have sufficient ties to the rare earth industry to make it a distinctive asset compared to other companies? Mark believes so but also thinks he was late to the party compared to other companies that had been lobbying in DC for a long time. He would have gotten federal funds before if he had been in that space earlier. They assembled a team that he says is best in class but that is usually the same song we hear from every executive in the junior mining business.

Divesting non-core assets

I must have been sleeping at the wheel when I listened to Matt on crux investor asking about this part as it came as a surprise to hear that they had a portfolio of smaller projects that they are in the last steps to divest to another company. This was quite interesting to hear because the impression I got was that is an integral part of the turnaround of the company instead of being active in the market to buy lbs of Uranium, which they won’t be do, or buying up other companies/projects. They believe that their non-core assets are of higher quality than most of what is being offered on the market currently. Why do I think this is in the last mile of finishing a deal? When asked if they would consider charging a toll for their mill to other companies, I had in mind Western Uranium which last I heard did not have such an agreement, Curtis said that in the past not but after the divestiture, they could potentially do it. You just had to be there to hear the dynamic between Mark and Curtis. We cannot/ will not talk about who will buy but we might entertain after..Maybe I misinterpreted the context but I wrote in my notes: Ur energy, Peninsula, Encore, Western are legitimate contenders to buy up these assets. Then, if we speculate, International consolidated Uranium, Azarga, and Mega uranium have this business model to buy project and try to package it to someone else later. Who do you have your money on?

Last thoughts, I seriously get a kick out of interviewing CEOs. The recording was not fantastic since both Marc and Curtis spoke extremely fast. Kudos to them to sustain this level of energy for the whole hour. Should I post the interview next time?

let me know in the comments!

Max